Generally, when we talk about professionals, we mean doctors, engineers, lawyers. So, when people hear of professional tax in organisations, they get curious. What this tax is all about?

Let’s walk you through some of the common questions about Professional Tax in this post.

What is professional tax and why it matter?

‘Professional tax’ is the name for a small recurring levy imposed by state governments on professions, trades, and employment. It is a tax on employees. The role of employers is only to deduct it from salaries each month and send it to the state.

Self-employed people pay it themselves. Each state sets its own rules about who should pay this tax, in what months, and exemptions if any.

As per regulation, Professional Tax (PT) is a state-level direct tax levied by state governments under Article 276 of the Constitution of India. (often called the Profession Tax Act).

It’s separate from income tax under the Income Tax Act and is collected by state Tax Departments or Commercial Taxes Departments.

The purpose behind PT is to raise revenue for state and local governments. It funds municipal services like health, education, public infrastructure. And supports local administration.

Scope and applicability of Professional Tax

Who must pay professional tax?

Here is a list of people and entities who must pay professional tax in India.

- Salaried employees and wage earners: Employers usually deduct professional tax from salary and remit it.

- Self-employed individuals and professionals: They must register and pay directly in many states (e.g., consultants, freelancers, insurance agents, medical diagnostic centers).

- Firms, HUFs and companies: Depending on state rules, such entities carrying on professions or business may have PT liabilities.

Professional Tax Slabs, Rates and Calculation Methodology

Professional Tax calculation isn’t same for all states. The PT follows a slab system. And each state sets its own professional tax slabs and slab rates. Some states levy a fixed monthly amount which is based on gross pay slabs. Others use annual assessment. A common minimum exemption seen in some states is around INR 2,500 monthly (state-specific — so it is a good idea to check your state details).

Let us see the examples of PT calculations for State of Maharashtra–

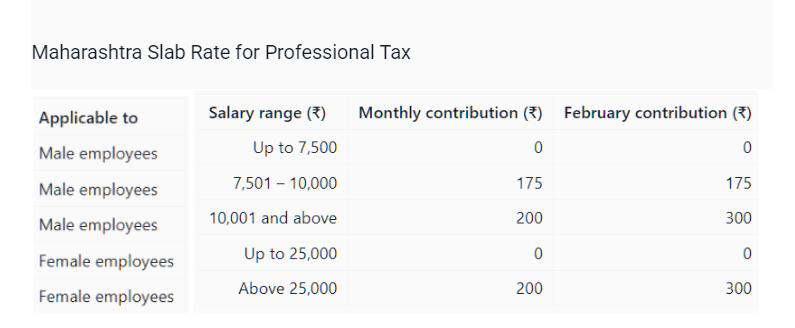

Maharashtra levies Professional Tax under the Maharashtra Labour Welfare Fund and Professional Tax Act (commonly administered by State Tax or Labour Department).

Maharashtra’s slabs set monthly rates with an annual maximum of Rs. 2,500.

Maharashtra professional tax — official slab as commonly applied–

- Monthly gross salary up to Rs. 7,499: Nil

- Monthly gross salary Rs. 7,500 to Rs. 9,999: Rs. 175 per month

- Monthly gross salary Rs. 10,000 and above: Rs. 200 per month (February Rs 300)

- Annual maximum: Rs. 2,500 (once cumulative deductions in a financial year reach Rs. 2,500, no further PT is deducted that year)

Important–

- In Maharshtra there are different slabs for male and female employees.

- For female employees with monthly gross salary upto rs 25,000 the PT is NIL.

Let us see how professional tax will be levied for a male employee in Maharashtra–

Example 1 — Regular full-year employee

- Monthly gross salary: Rs. 6,500

- Slab: Up to Rs. 7,499 → Nil

- Monthly PT = Rs. 0

- Annual PT = Rs. 0

Example 2 — Mid-range salary

- Monthly gross salary: Rs. 8,500

- Slab: Rs. 7,500–9,999 → Rs. 175 per month

- Monthly PT = Rs. 175

- Annual PT = 175 × 12 = Rs. 2,100

Example 3 — Salary hitting higher slab and annual cap

- Monthly gross salary: Rs. 60,000

- Slab: Rs. 10,000 and above → Rs. 200 per month

- Monthly PT = Rs. 200

- Annual PT = 200 × 12 = Rs. 2,400 (+ February 100) = 2500

Professional Tax registration, certificates and identification

It’s mandatory for employers to register and obtain a Professional Tax Registration Number.

Self-employed professionals should get a Professional Tax enrolment certificate or registration certificate depending on the specific requirement in their state.

Registration is easy with documents like proof of Identity, PAN, address proof, proof of business or profession, and employee details for employers.

To get their PT registration one can visit State Tax Department or Commercial Taxes Department portals. Or their designated offices.

Employer obligations and payroll

Usually, employers deduct professional tax from employees and remit it to the respective state authority. Therefore, their role is significant in the collection of PT and ensuring compliance. Payroll management software helps automate these deductions and streamline adherence to state-specific regulations.

Here are the employer duties:

- Deduct professional tax from employees’ salaries at the applicable rate.

- Show the deduction clearly on salary slips (and on Form 16/Form 16A if required)

- Remit the deducted tax to the state authority within the prescribed timelines

- File periodic professional tax returns or forms as specified by the state.

- Keep accurate records and supporting documents for audits and compliance checks.

- Monitor state-specific rules (rates, thresholds, filing formats and timelines) and update payroll process accordingly.

- Ensure timely payment and filing to avoid interest, penalties and additional tax liabilities.

Professional Tax: exemptions, concessions and special categories

States often offer targeted exemptions and concessions to protect vulnerable groups and to keep essential services affordable.

- Disability and welfare: States often provide exemptions or concessions for persons with disabilities and for certain welfare groups.

- Low-income thresholds: Some states exempt those below a monetary threshold. It is shown in the state’s slab chart.

- Profession-specific rules: Certain professions like legal practitioners, broadcasting service providers, petrol/diesel/gas filling stations, may have tailored provisions.

How Professional tax relate with income tax and other levies?

Professional tax is different from the income tax charged under the Income Tax Act (Income Tax Act of 1961). PT is not a central direct tax but a state-level levy.

Deduction claims:

Typically professional tax paid by an individual may be allowed as a deduction under the income tax rules in some contexts — check the Income Tax Act and current practice.

Notice the state-differences regarding PT slabs and its enforcement

Slabs, registration and enforcement vary by state — Tamil Nadu, West Bengal, Andhra Pradesh, Maharashtra and Karnataka each have different rules.

- Departments and portals: Most states use their Commercial Tax Department or a state Tax Department portal for registration, payment and returns. Follow your state’s guidelines.

- Forms and IDs: States have unique form names/IDs (downloadable from portals).

Penalties, enforcement and dispute resolution

Non adherence to professional tax compliance can attract penalties and even prosecution or forced recovery. So the employers must not ignore it.

Penalties: Here are some common penalty scenarios–

- Late registration fines

- Failure to deduct: interest and penalties on unpaid tax

- Late remittance: interest and late-payment penalties

- Incorrect filing: fines per return or percentage-based penalties

- Failure to issue certificates: monetary fines

- Criminal prosecution in severe evasion cases (rare)

- Penalties are often cumulative: interest + fixed fines + potential audits

Forced Recovery: Outstanding professional tax can be recovered by attachment of property or other measures as per state law.

Appeals: Assessment orders can be challenged in prescribed appellate forums under state statutes.

Practical checklist for compliance (for employers and professionals)

- Verify if your state requires registration for your role or entity.

- Obtain the Professional Tax Registration Number and keep the Registration Certificate accessible.

- Update payroll software to reflect state slab rates and deduct Professional Tax correctly on pay slips.

- File periodic returns and remit tax online before the due date to avoid interest and penalties.

- Keep proof of payments and registration for at least the period required by state law.

- For freelancers and self-employed professionals: calculate monthly/annual slab liability and remit via the designated state portal.

Some professional tax scenarios are not as simple as shown above. In today’s interconnected world new scenarios can arise. In such cases an expert opinion is a must.

Cross-state employees, remote work across states, high-value professionals and businesses with multiple establishments should seek Tax Consultants or RCC Consultants.

Professional tax is small in amount but big in impact.

It affects payroll compliance, take-home pay and pricing for freelancers and contractors. For employees it’s a routine deduction that must be checked on payslips; for freelancers and contractors it can mean a local registration and periodic payments.

For employers it’s a recurring compliance duty — deduct correctly, file on time and keep records.

The rules vary by state: rates, slabs, exemptions and filing dates differ, so one must treat state law as the source of truth.

FAQs About Professional Tax in India

01

Can two states tax the same person?Generally, the state where employment is exercised or business is carried out has jurisdiction; cross-state situations can be complex and need advice.

02

Is Professional tax shown in Form 16?Salary deductions like professional tax are often reflected on Form 16/Form 16A as necessary.

03

Which state’s PT applies if employer is in one state and employee works in another?The state where the employee performs services generally applies. For employees working remotely from their home state for an employer based elsewhere, many states require the PT for the state of the employee’s work location.

04

How professional tax is levied if employees are posted to multiple states in a year? Employers must allocate PT based on posting location and ensure correct deductions for each period.

05

Do interns or apprentices attract professional tax?Usually not for unpaid interns.

For paid interns and apprentices: yes, if their stipend or salary exceeds the state’s taxable slab or if the state law treats them as employees. State rules vary — check the specific state notification.

How professional tax is treated for for non‑resident employees or foreign nationals

PT liability depends on the state where the service is exercised — not strictly on residency.

Foreign nationals or non‑resident employees who perform work in an Indian state usually attract that state’s professional tax for the period they work there (if income exceeds slabs).

Short temporary visits may still create a PT obligation if the state law has no minimum days rule.

06

Are refunds possible for professional tax? PT overpayments can be claimed as refunds via the state procedure.

07

How long one should keep PT records?Keep records as required by state law and for income tax assessments. The usual practice is to keep it for several years.

Visited 278 times

Visited 278 times